Payment rails explained: security risks in real estate

Legacy payment infrastructure wasn't built for digital fraud. Here's why every wire transfer puts your business at risk—and what's replacing it.

Share article:

.png)

Cheryl Crouse

8 minutes

Digital Payments

Nov 24, 2025

Mar 10, 2026

A title company processes what seems like a routine mortgage payoff wire. Instructions came via email from a familiar lender address. The callback number checked out. The wire goes through. Three days later, they discover the $276,000 went to fraudsters. And they're 100% liable.

This scenario played out hundreds of times in 2024. According to CertifID's State of Wire Fraud 2025 report, fraud losses averaged $68k for buyer funds, $172k for seller proceeds, and $276k for mortgage payoffs.

The culprit? Payment rails built when bankers knew customers by name. Today, digital communication has separated instruction delivery from payment execution—creating a gap fraudsters exploit daily.

What are payment rails?

Payment rails are the infrastructure and networks that move money between parties in real estate transactions. They include systems like ACH, wire transfers (SWIFT), and card networks that handle earnest money, cash-to-close funds, seller proceeds, and payoffs.

Think of them as the tracks money travels on—they execute whatever instructions they receive without verifying authenticity. This vulnerability is why wire fraud happens and why verification must occur before funds move.

Key aspects of payment rails

- Infrastructure: The systems connecting financial institutions to enable secure fund transfers

- Function: Handle all transaction types, from earnest money deposits to international wire transfers

- Vulnerability: Execute instructions without questioning source or authenticity—explaining why wire fraud happens

- Evolution: Moving toward verification-first infrastructure where identity checks are built into the transfer process, not added afterward

How payment rails work in real estate closings

Every real estate transaction includes multiple moments when payment information moves between parties. These handoff points create vulnerabilities in the payment flow.

The payment flow in a typical real estate transaction

The payment journey involves multiple moving parts. Earnest money deposits operate under tight timelines. Digital payments complete in minutes versus days for traditional wires.

According to our data, cash-to-close funds carry a median fraud value of $68,413 (30% of all fraud cases).

Seller proceeds show median losses of $172,080 (12% of cases).

Mortgage payoff wires represent the highest-risk payment type: median fraud value of $275,927, accounting for 48% of all fraud recovery cases.

The critical handoff points where fraud occurs

Wire instructions arrive via email—the most vulnerable point.

Manual verification attempts include callbacks that can be spoofed, visual ID checks that fail, and inadequate documentation.

These manual checks miss the fundamental problem: payment rails are "dumb infrastructure." They execute whatever instructions they receive without questioning authenticity.

Fraudsters simultaneously hit companies across various States within days, exploiting the same vulnerabilities. Payment rails process every fraudulent wire because they can't distinguish legitimate from fraudulent instructions.

Types of payment rails used in real estate

Understanding the different payment rails helps you see where vulnerabilities exist and why the infrastructure itself creates risk.

Traditional wire transfers (Fedwire, SWIFT)

Bank-to-bank electronic transfers work through federal or international networks. Same-day or next-day settlement comes with typical costs of $15-30 per wire. The speed advantage makes wires the default choice for closing transactions.

The fraud vulnerability? Zero built-in identity verification at the infrastructure level. This connects directly to the median mortgage payoff fraud loss of $275,927—48% of all fraud recovery cases involve payoff wires. When fraudsters intercept instructions, the wire executes without questioning authenticity.

Larger financial institutions have different routing numbers for wires versus ACH, creating verification complications. Your team must track multiple numbers for the same institution, increasing the chance of errors.

.png)

ACH transfers

ACH processing takes 1-3 business days with costs of $0.50-$3 per transaction. Adoption is limited because transfers are perceived as "too slow" for time-sensitive transactions. The same vulnerability exists: no identity verification built into the rail itself.

The return risk problem creates operational headaches. Funds credited to escrow can fail or bounce days later, disrupting closings and creating reconciliation work. Most digital payment vendors require customers to handle 100% of post-credit return reconciliation.

Modern platforms like CertifID address this by assuming all ACH return risk once funds credit your escrow account. A two-business-day delivery captures 95%+ of ACH returns before they become your problem. After that window, credited funds are final—no clawbacks, no reconciliation.

Paper checks

Some law firms issue paper checks for 99% of seller proceeds despite obvious drawbacks. The manual processing burden includes bank visits, physical delivery, and multi-day clearing times. Fraud risks include check washing, forgery, and altered amounts.

RTP and FedNow: Emerging digital payment rails

Real-time settlement provides instant payment confirmation. Both The Clearing House's RTP network and the Federal Reserve's FedNow Service can handle high-value transactions, with rising limits as of 2025.

The challenge isn't the rails themselves—RTP and FedNow work fine. The issue is bank participation. Not every financial institution supports these rails yet.

Platforms that automatically detect a buyer's bank capabilities during account setup help close this gap. If the buyer's bank supports Instant payment via RTP or FedNow, the system can route through these rails while maintaining the same fraud protection and fund finality guarantees.

Why legacy payment rails fail: the modern fraud threat

The payment infrastructure supporting real estate transactions wasn't designed for today's threat landscape.

Understanding why these systems fail requires looking at both their historical context and the sophisticated attacks exploiting them daily.

Payment rails were built for a different threat landscape

Wire transfer infrastructure was designed in the 1970s-1980s when in-person banking was standard. Banks knew their customers through face-to-face relationships and verified identities at the branch level. Wire instructions were delivered on paper, in person, or via phone to known contacts. This was the pre-email reality.

Digital communication separated instruction delivery from payment execution. This created the vulnerability window that fraudsters now exploit daily.

The rails themselves remained unchanged. They're still just transportation systems moving money based on instructions received. They have no ability to verify the authenticity of those instructions.

The dangerous gap between verification and execution

This gap occurs between receiving wire instructions via email and executing the wire transfer. The FBI reports BEC is now a $50 billion scam industry, with real estate transactions as a primary target.

APIs aggregate property records for just a few hundred dollars monthly, giving fraudsters access to thousands of potential targets. AI-powered targeting analyzes data to develop more targeted attacks. Pattern recognition enables continual improvement in impersonation via text, email, voice, and video.

According to our data, once a company experiences one high-risk transaction, their rate of high-risk transactions rises up to 6x higher than peer companies. This pattern suggests fraudsters maintain detailed target lists and return to companies they’ve successfully compromised.

Business email compromise and coordinated attacks

Fraudsters intercept transaction communications and modify wire instructions. They operate at an industrial scale. CertifID works with people who've been tricked. Fraudsters scale attacks to hit 50, 100, or 200 different title companies simultaneously, "hoping just one employee veers from protocol on a closing."

The same criminal groups execute coordinated attacks across multiple states within days. Criminals are hitting law firms in South Carolina, escrow teams in Southern California, and title companies in Minnesota using identical compromise tactics.

The payment rails process every fraudulent wire because they can't distinguish between legitimate and fraudulent instructions.

Mortgage payoff fraud: the highest-risk payment type

Payoff wires are the top target because they come directly from company escrow accounts, creating direct liability with no shared responsibility.

The median fraud value of $275,927 represents 48% of all fraud recovery cases. Teams describe payoff wires as "the smoking gun"—if funds go to the wrong spot, "you're directly liable for that."

Why manual verification methods aren't enough

Phone callbacks can be spoofed. It's "no longer possible for a business to rely on human efforts to catch communications that are slightly 'off' or inspect IDs against a multi-point checklist."

Real example from customer transcripts: "verified with Bill, no last name on 2/26"—inadequate documentation when wires go wrong.

Generative AI accelerates the problem: fraudsters continuously improve impersonation across all communication channels.

The liability asymmetry that threatens businesses

Title companies and law firms bear 100% liability exposure for misdirected wires. Most title agencies operate on 10-20% profit margins, so one $276k payoff fraud can close the business permanently.

According to our data, 29% of title companies spend less than $1k annually on fraud prevention, and 20% spend zero. Yet 28% of title companies reported having at least one customer send funds to the wrong place due to fraud in 2024.

Compliance and regulatory pressure escalating

ALTA best practices, SOC 2 compliance demands, and varying state-specific regulations create mounting pressure. Courts increasingly expect higher standards of care from title companies and law firms. Understanding who is liable shows the stakes clearly.

First-time real estate consumers fall victim at 3x the rate of experienced buyers (7.5% vs. 2.3%). The gap between legacy infrastructure and modern security needs isn't just a technical problem but a business survival issue.

Benefits of modern payment rails with integrated verification

The next generation of payment infrastructure verifies identity before executing transactions, not after.

Identity verification at the payment rail level

Modern payment rails integrate identity verification directly into the payment flow. Before accepting wire instructions, these systems verify identity through device authentication, multi-factor verification, and account validation.

Title companies operating in strict good funds states—like Texas, California, and New York—can now accept earnest money digitally while staying compliant. The solution: buyers initiate payment digitally via ACH, but title companies receive funds via Wire or Instant payment rails—both widely recognized as meeting good funds requirements.

Unlike traditional systems that blindly execute instructions, verification-first infrastructure confirms who's sending instructions before moving money. Verifying wire instructions becomes automated rather than manual.

How flexible payment configuration works

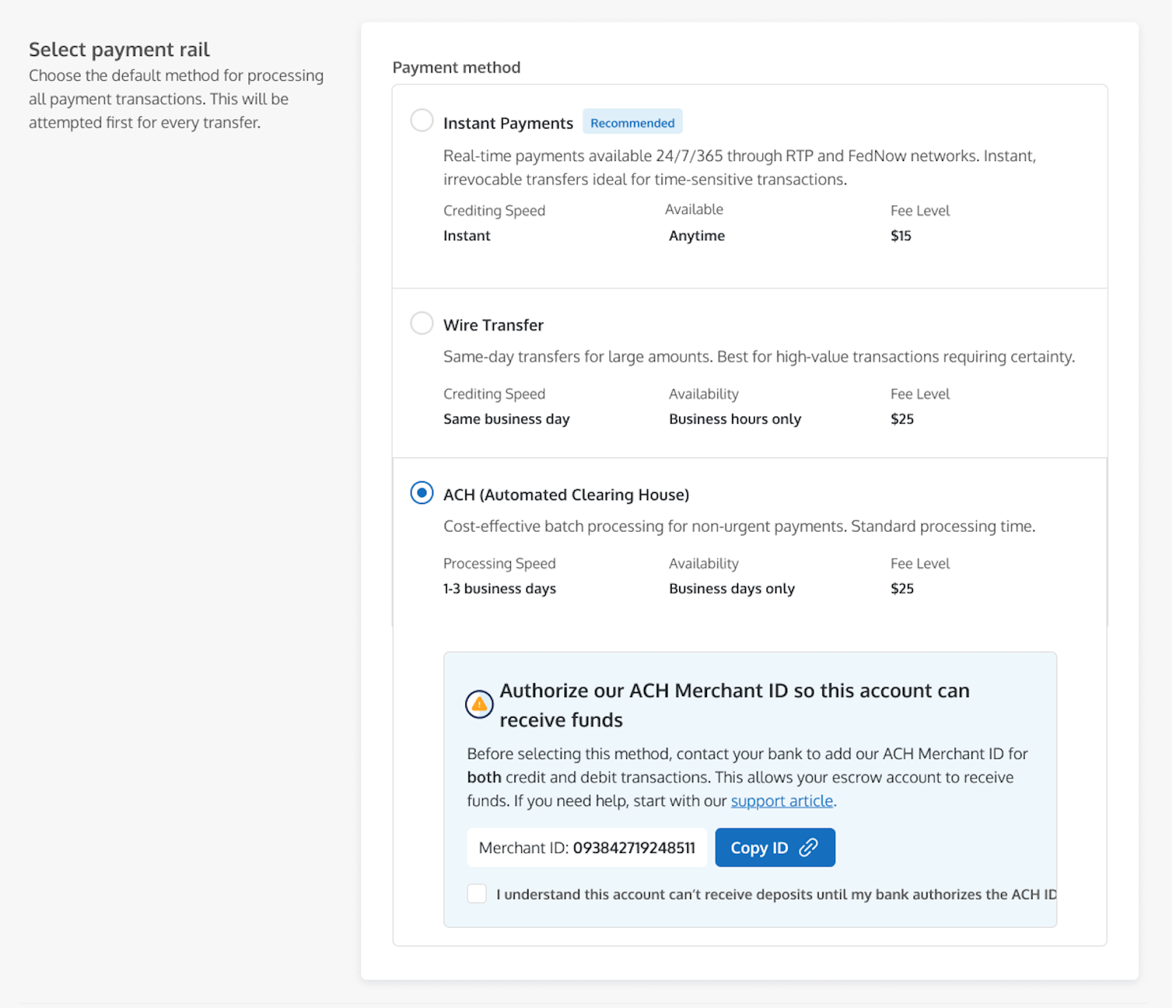

You get three ways to accept earnest money deposits: ACH, Instant (RTP/FedNow), or Wire delivery. The configuration matches your operating policies, compliance requirements, and risk tolerance.

Here's the setup process:

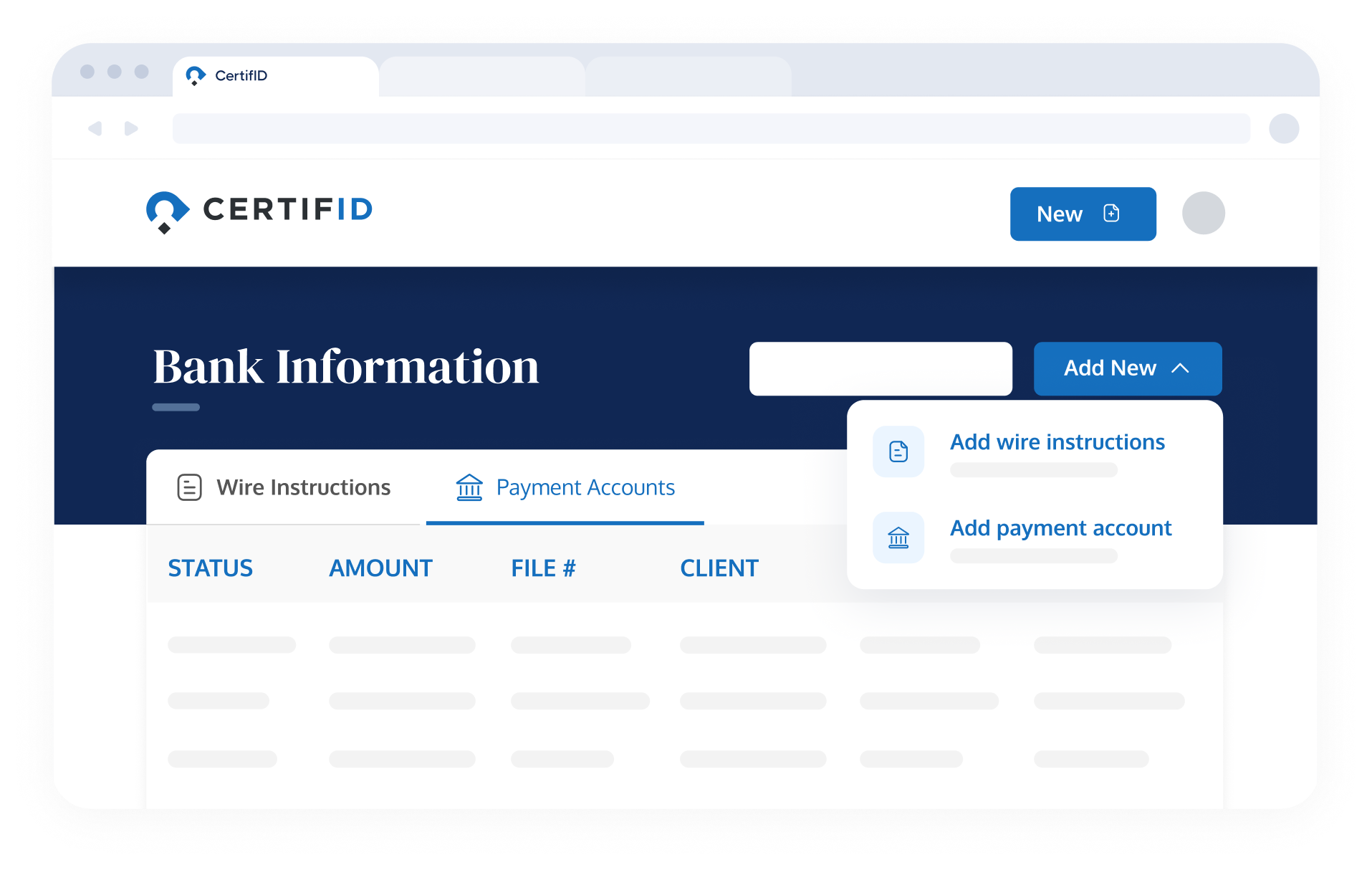

During onboarding, you configure your payment account by selecting your preferred transfer type.

You'll add your bank information—display name, routing number, account number—and choose between "Instant Payment with RTP and FedNow", Wire, or "ACH (Automated Clearing House)." This configuration applies across your entire company.

Once configured, you send buyers a branded payment link via text and email. They complete identity verification (KYC, device authentication, multi-factor verification) and add their bank account details.

The two-business-day delivery captures 95%+ of ACH returns before funds hit your escrow account. Once funds credit, they're final—no clawbacks, no reconciliation. You're protected from post-credit return risk entirely.

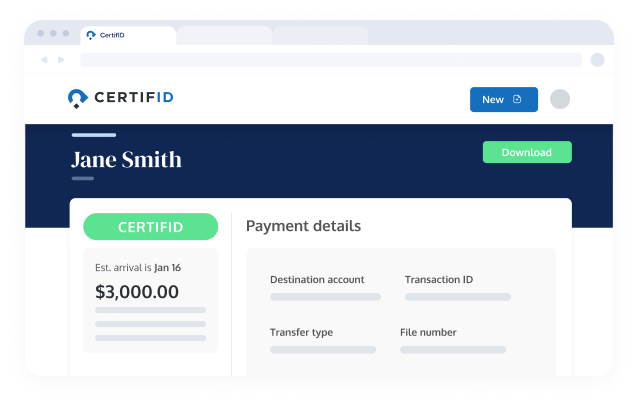

You see instant payment status and complete metadata—buyer name, address, contact info, payment details—so you can immediately apply funds to the correct file. Your buyers pay $20 for ACH or Instant, $28 for Wire—significantly less than traditional wire costs. You get compliance-friendly payment rails with guaranteed fund finality.

Network intelligence and competitive advantage

Verification-first rails create network effects through pattern recognition across thousands of transactions. When fraudsters launch coordinated attacks in one state, the system flags similar attempts across the network—collective defense versus individual battles.

The market is moving

Large national clients expect advanced payment infrastructure as a baseline. Millennials (ages 25-44), the largest homebuyer segment, expect mobile-first experiences. Wire transfers feel foreign to buyers. But an online payment makes sense.

More than half of buyers choose digital payment portals when given the option. Integration with title production software makes the transition seamless.

The future of payment rails in real estate

Payment rails themselves work fine. The problem is outdated verification systems that can't keep pace with sophisticated fraud tactics. Here's what the next generation of payment infrastructure looks like for secure, efficient closings.

Real-time payment networks (RTP, FedNow)

Real-time payment rails are no longer just a future option for real estate—they're live. Title companies can now configure earnest money deposits to deliver via RTP or FedNow, offering instant settlement alongside the same fraud protection and fund finality guarantees.

The remaining challenge is bank participation. Platforms that automatically verify if a buyer's bank supports RTP or FedNow during account setup help close this gap. The system highlights Instant payment as an option when available, with educational copy explaining the speed and cost benefits.

Verification-first payment infrastructure

The shift to identity verification as a core feature built into the rail represents the next evolution. Fraudsters use generative AI to continuously improve impersonation. Defense systems must match this sophistication.

The three-configuration model (ACH, Instant, Wire) demonstrates this evolution. Every configuration includes the same fraud protection suite: identity verification through KYC, account validation, balance checks, real-time fraud detection, and Trust and Safety manual review when needed. All transactions are fully insured.

Industry standardization and network effects

Movement toward unified security standards continues. The ability to identify cross-company fraud patterns will become essential. Secure online transactions will become standard.

As more title companies adopt configurable payment rails with built-in verification, the collective defense strengthens. Fraudsters hitting one company trigger alerts across the entire network.

Payment rails security: protect your customers and business

Legacy payment rails create a dangerous gap between identity verification and payment execution. Criminals use AI, APIs, and generative technology to scale attacks.

79% of consumers demand better security, courts expect higher standards of care, and average fraud losses of $68k-$276k far exceed prevention costs.

Title companies processing 300+ closings monthly need enterprise fraud prevention software. Integration with SoftPro ensures your team doesn't need to change workflows.

Stay ahead of evolving fraud threats by subscribing to CertifID's newsletter.

FAQ

Do buyers need to download an app or create an account?

No. Buyers receive a branded payment link via text and email. They click it, complete verification on their phone or computer, and submit their bank details—all through a web browser. No downloads, no logins, no passwords to remember. Fees are disclosed upfront before submission, and if a bank holiday will delay processing, buyers see a notification explaining the delay and when funds will resume moving—so no one is left guessing.

What's the actual implementation time for verified payment rails?

Integration with title production software like SoftPro, ResWare, and RamQuest typically takes under an hour. Your team doesn't need training on a new system. Verified rails work within your existing workflow. You send payment links the same way you'd send any transaction communication.

What happens when a buyer is traveling or living out of state?

Digital payment rails work from anywhere in the US. However, if verification attempts occur outside the country, the system automatically flags and fails the transaction—too risky. This actually protects you from a common fraud scenario where someone claims to be "on vacation" while attempting to intercept funds.

How do I choose between ACH, Instant, and Wire configurations?

Ask yourself two questions: First, does your state require good funds for earnest money? Second, what's your company's policy on accepting ACH payments?

If you operate in strict good funds states (TX, CA, NY), choose Instant or Wire configurations. Buyers still initiate payment digitally via ACH, but you receive funds via Instant payment or Wire—both widely recognized as meeting good funds standards.

If your state allows ACH but you want to eliminate return risk, any configuration works. All three include the two-day delivery period and guaranteed fund finality—no clawbacks, no reconciliation. The beauty: you can start with one configuration and switch later if your needs change.

Senior Product Manager

Cheryl brings nearly a decade of product management experience in the real estate industry, making her mark at both scrappy startups and well-established companies. Driven by a deep customer focus and love for technology, she’s helped build innovative solutions that keep pace with evolving needs. At CertifID, Cheryl is helping drive the next phase of growth and push forward the mission to create a world without wire fraud.

A title company processes what seems like a routine mortgage payoff wire. Instructions came via email from a familiar lender address. The callback number checked out. The wire goes through. Three days later, they discover the $276,000 went to fraudsters. And they're 100% liable.

This scenario played out hundreds of times in 2024. According to CertifID's State of Wire Fraud 2025 report, fraud losses averaged $68k for buyer funds, $172k for seller proceeds, and $276k for mortgage payoffs.

The culprit? Payment rails built when bankers knew customers by name. Today, digital communication has separated instruction delivery from payment execution—creating a gap fraudsters exploit daily.

What are payment rails?

Payment rails are the infrastructure and networks that move money between parties in real estate transactions. They include systems like ACH, wire transfers (SWIFT), and card networks that handle earnest money, cash-to-close funds, seller proceeds, and payoffs.

Think of them as the tracks money travels on—they execute whatever instructions they receive without verifying authenticity. This vulnerability is why wire fraud happens and why verification must occur before funds move.

Key aspects of payment rails

- Infrastructure: The systems connecting financial institutions to enable secure fund transfers

- Function: Handle all transaction types, from earnest money deposits to international wire transfers

- Vulnerability: Execute instructions without questioning source or authenticity—explaining why wire fraud happens

- Evolution: Moving toward verification-first infrastructure where identity checks are built into the transfer process, not added afterward

How payment rails work in real estate closings

Every real estate transaction includes multiple moments when payment information moves between parties. These handoff points create vulnerabilities in the payment flow.

The payment flow in a typical real estate transaction

The payment journey involves multiple moving parts. Earnest money deposits operate under tight timelines. Digital payments complete in minutes versus days for traditional wires.

According to our data, cash-to-close funds carry a median fraud value of $68,413 (30% of all fraud cases).

Seller proceeds show median losses of $172,080 (12% of cases).

Mortgage payoff wires represent the highest-risk payment type: median fraud value of $275,927, accounting for 48% of all fraud recovery cases.

The critical handoff points where fraud occurs

Wire instructions arrive via email—the most vulnerable point.

Manual verification attempts include callbacks that can be spoofed, visual ID checks that fail, and inadequate documentation.

These manual checks miss the fundamental problem: payment rails are "dumb infrastructure." They execute whatever instructions they receive without questioning authenticity.

Fraudsters simultaneously hit companies across various States within days, exploiting the same vulnerabilities. Payment rails process every fraudulent wire because they can't distinguish legitimate from fraudulent instructions.

Types of payment rails used in real estate

Understanding the different payment rails helps you see where vulnerabilities exist and why the infrastructure itself creates risk.

Traditional wire transfers (Fedwire, SWIFT)

Bank-to-bank electronic transfers work through federal or international networks. Same-day or next-day settlement comes with typical costs of $15-30 per wire. The speed advantage makes wires the default choice for closing transactions.

The fraud vulnerability? Zero built-in identity verification at the infrastructure level. This connects directly to the median mortgage payoff fraud loss of $275,927—48% of all fraud recovery cases involve payoff wires. When fraudsters intercept instructions, the wire executes without questioning authenticity.

Larger financial institutions have different routing numbers for wires versus ACH, creating verification complications. Your team must track multiple numbers for the same institution, increasing the chance of errors.

ACH transfers

ACH processing takes 1-3 business days with costs of $0.50-$3 per transaction. Adoption is limited because transfers are perceived as "too slow" for time-sensitive transactions. The same vulnerability exists: no identity verification built into the rail itself.

The return risk problem creates operational headaches. Funds credited to escrow can fail or bounce days later, disrupting closings and creating reconciliation work. Most digital payment vendors require customers to handle 100% of post-credit return reconciliation.

Modern platforms like CertifID address this by assuming all ACH return risk once funds credit your escrow account. A two-business-day delivery captures 95%+ of ACH returns before they become your problem. After that window, credited funds are final—no clawbacks, no reconciliation.

Paper checks

Some law firms issue paper checks for 99% of seller proceeds despite obvious drawbacks. The manual processing burden includes bank visits, physical delivery, and multi-day clearing times. Fraud risks include check washing, forgery, and altered amounts.

RTP and FedNow: Emerging digital payment rails

Real-time settlement provides instant payment confirmation. Both The Clearing House's RTP network and the Federal Reserve's FedNow Service can handle high-value transactions, with rising limits as of 2025.

The challenge isn't the rails themselves—RTP and FedNow work fine. The issue is bank participation. Not every financial institution supports these rails yet.

Platforms that automatically detect a buyer's bank capabilities during account setup help close this gap. If the buyer's bank supports Instant payment via RTP or FedNow, the system can route through these rails while maintaining the same fraud protection and fund finality guarantees.

Why legacy payment rails fail: the modern fraud threat

The payment infrastructure supporting real estate transactions wasn't designed for today's threat landscape.

Understanding why these systems fail requires looking at both their historical context and the sophisticated attacks exploiting them daily.

Payment rails were built for a different threat landscape

Wire transfer infrastructure was designed in the 1970s-1980s when in-person banking was standard. Banks knew their customers through face-to-face relationships and verified identities at the branch level. Wire instructions were delivered on paper, in person, or via phone to known contacts. This was the pre-email reality.

Digital communication separated instruction delivery from payment execution. This created the vulnerability window that fraudsters now exploit daily.

The rails themselves remained unchanged. They're still just transportation systems moving money based on instructions received. They have no ability to verify the authenticity of those instructions.

The dangerous gap between verification and execution

This gap occurs between receiving wire instructions via email and executing the wire transfer. The FBI reports BEC is now a $50 billion scam industry, with real estate transactions as a primary target.

APIs aggregate property records for just a few hundred dollars monthly, giving fraudsters access to thousands of potential targets. AI-powered targeting analyzes data to develop more targeted attacks. Pattern recognition enables continual improvement in impersonation via text, email, voice, and video.

According to our data, once a company experiences one high-risk transaction, their rate of high-risk transactions rises up to 6x higher than peer companies. This pattern suggests fraudsters maintain detailed target lists and return to companies they’ve successfully compromised.

Business email compromise and coordinated attacks

Fraudsters intercept transaction communications and modify wire instructions. They operate at an industrial scale. CertifID works with people who've been tricked. Fraudsters scale attacks to hit 50, 100, or 200 different title companies simultaneously, "hoping just one employee veers from protocol on a closing."

The same criminal groups execute coordinated attacks across multiple states within days. Criminals are hitting law firms in South Carolina, escrow teams in Southern California, and title companies in Minnesota using identical compromise tactics.

The payment rails process every fraudulent wire because they can't distinguish between legitimate and fraudulent instructions.

Mortgage payoff fraud: the highest-risk payment type

Payoff wires are the top target because they come directly from company escrow accounts, creating direct liability with no shared responsibility.

The median fraud value of $275,927 represents 48% of all fraud recovery cases. Teams describe payoff wires as "the smoking gun"—if funds go to the wrong spot, "you're directly liable for that."

Why manual verification methods aren't enough

Phone callbacks can be spoofed. It's "no longer possible for a business to rely on human efforts to catch communications that are slightly 'off' or inspect IDs against a multi-point checklist."

Real example from customer transcripts: "verified with Bill, no last name on 2/26"—inadequate documentation when wires go wrong.

Generative AI accelerates the problem: fraudsters continuously improve impersonation across all communication channels.

The liability asymmetry that threatens businesses

Title companies and law firms bear 100% liability exposure for misdirected wires. Most title agencies operate on 10-20% profit margins, so one $276k payoff fraud can close the business permanently.

According to our data, 29% of title companies spend less than $1k annually on fraud prevention, and 20% spend zero. Yet 28% of title companies reported having at least one customer send funds to the wrong place due to fraud in 2024.

Compliance and regulatory pressure escalating

ALTA best practices, SOC 2 compliance demands, and varying state-specific regulations create mounting pressure. Courts increasingly expect higher standards of care from title companies and law firms. Understanding who is liable shows the stakes clearly.

First-time real estate consumers fall victim at 3x the rate of experienced buyers (7.5% vs. 2.3%). The gap between legacy infrastructure and modern security needs isn't just a technical problem but a business survival issue.

Benefits of modern payment rails with integrated verification

The next generation of payment infrastructure verifies identity before executing transactions, not after.

Identity verification at the payment rail level

Modern payment rails integrate identity verification directly into the payment flow. Before accepting wire instructions, these systems verify identity through device authentication, multi-factor verification, and account validation.

Title companies operating in strict good funds states—like Texas, California, and New York—can now accept earnest money digitally while staying compliant. The solution: buyers initiate payment digitally via ACH, but title companies receive funds via Wire or Instant payment rails—both widely recognized as meeting good funds requirements.

Unlike traditional systems that blindly execute instructions, verification-first infrastructure confirms who's sending instructions before moving money. Verifying wire instructions becomes automated rather than manual.

How flexible payment configuration works

You get three ways to accept earnest money deposits: ACH, Instant (RTP/FedNow), or Wire delivery. The configuration matches your operating policies, compliance requirements, and risk tolerance.

Here's the setup process:

During onboarding, you configure your payment account by selecting your preferred transfer type.

You'll add your bank information—display name, routing number, account number—and choose between "Instant Payment with RTP and FedNow", Wire, or "ACH (Automated Clearing House)." This configuration applies across your entire company.

Once configured, you send buyers a branded payment link via text and email. They complete identity verification (KYC, device authentication, multi-factor verification) and add their bank account details.

The two-business-day delivery captures 95%+ of ACH returns before funds hit your escrow account. Once funds credit, they're final—no clawbacks, no reconciliation. You're protected from post-credit return risk entirely.

You see instant payment status and complete metadata—buyer name, address, contact info, payment details—so you can immediately apply funds to the correct file. Your buyers pay $20 for ACH or Instant, $28 for Wire—significantly less than traditional wire costs. You get compliance-friendly payment rails with guaranteed fund finality.

Network intelligence and competitive advantage

Verification-first rails create network effects through pattern recognition across thousands of transactions. When fraudsters launch coordinated attacks in one state, the system flags similar attempts across the network—collective defense versus individual battles.

The market is moving

Large national clients expect advanced payment infrastructure as a baseline. Millennials (ages 25-44), the largest homebuyer segment, expect mobile-first experiences. Wire transfers feel foreign to buyers. But an online payment makes sense.

More than half of buyers choose digital payment portals when given the option. Integration with title production software makes the transition seamless.

The future of payment rails in real estate

Payment rails themselves work fine. The problem is outdated verification systems that can't keep pace with sophisticated fraud tactics. Here's what the next generation of payment infrastructure looks like for secure, efficient closings.

Real-time payment networks (RTP, FedNow)

Real-time payment rails are no longer just a future option for real estate—they're live. Title companies can now configure earnest money deposits to deliver via RTP or FedNow, offering instant settlement alongside the same fraud protection and fund finality guarantees.

The remaining challenge is bank participation. Platforms that automatically verify if a buyer's bank supports RTP or FedNow during account setup help close this gap. The system highlights Instant payment as an option when available, with educational copy explaining the speed and cost benefits.

Verification-first payment infrastructure

The shift to identity verification as a core feature built into the rail represents the next evolution. Fraudsters use generative AI to continuously improve impersonation. Defense systems must match this sophistication.

The three-configuration model (ACH, Instant, Wire) demonstrates this evolution. Every configuration includes the same fraud protection suite: identity verification through KYC, account validation, balance checks, real-time fraud detection, and Trust and Safety manual review when needed. All transactions are fully insured.

Industry standardization and network effects

Movement toward unified security standards continues. The ability to identify cross-company fraud patterns will become essential. Secure online transactions will become standard.

As more title companies adopt configurable payment rails with built-in verification, the collective defense strengthens. Fraudsters hitting one company trigger alerts across the entire network.

Payment rails security: protect your customers and business

Legacy payment rails create a dangerous gap between identity verification and payment execution. Criminals use AI, APIs, and generative technology to scale attacks.

79% of consumers demand better security, courts expect higher standards of care, and average fraud losses of $68k-$276k far exceed prevention costs.

Title companies processing 300+ closings monthly need enterprise fraud prevention software. Integration with SoftPro ensures your team doesn't need to change workflows.

Stay ahead of evolving fraud threats by subscribing to CertifID's newsletter.

Senior Product Manager

Cheryl brings nearly a decade of product management experience in the real estate industry, making her mark at both scrappy startups and well-established companies. Driven by a deep customer focus and love for technology, she’s helped build innovative solutions that keep pace with evolving needs. At CertifID, Cheryl is helping drive the next phase of growth and push forward the mission to create a world without wire fraud.

Sign up for The Wire to join the conversation.

.png)

Austin

3601 South Congress Ave.

Ste D200, Austin, Texas 78704

Grand Rapids

124 Fulton Street E

Grand Rapids, MI 49503